fiscal buffering or bust

tl;dr: raising interest rates will hurt, not help, inflation by making it more difficult to build the capacity required to rebound from ongoing supply shocks. benefits from the inflation reduction act, chips act, etc. will not show up for years. we need to establish federal emergency management of more pce indicators beyond just energy (i.e. the spr but for food, housing, and more).

***

the fed just did its fifth rate increase this year. word on the street is that it will continue doing these every few months until it gets its overnight rate above 5%. there’s a particular set of economic assumptions behind this that seem to make a lot of sense to markets, but which puzzle me.

the theory of how monetary policy fights inflation is simple. it’s supposed to work via wage-price dynamics: higher borrowing costs lead to less corporate investment and hiring, which leads to less bidding up of wages, which requires less raising of prices to maintain margin, which eases pressure to bid up wages—thus stopping the cycle.

in practice i fear it is currently working something like this: high inflation is causing interest rate increases, which negatively impacts asset prices. this leads to lower executive compensation and net worth, which is a very good way to get executives to do whatever the street says is needed in order to make the fed stop raising rates. so they cut costs, and inevitably, jobs. this might get papered over in analyst calls with talk of increased focus on cash flows, but it’s hard not to hear it like a plea to get back to a low-interest-rate world where line only goes up.

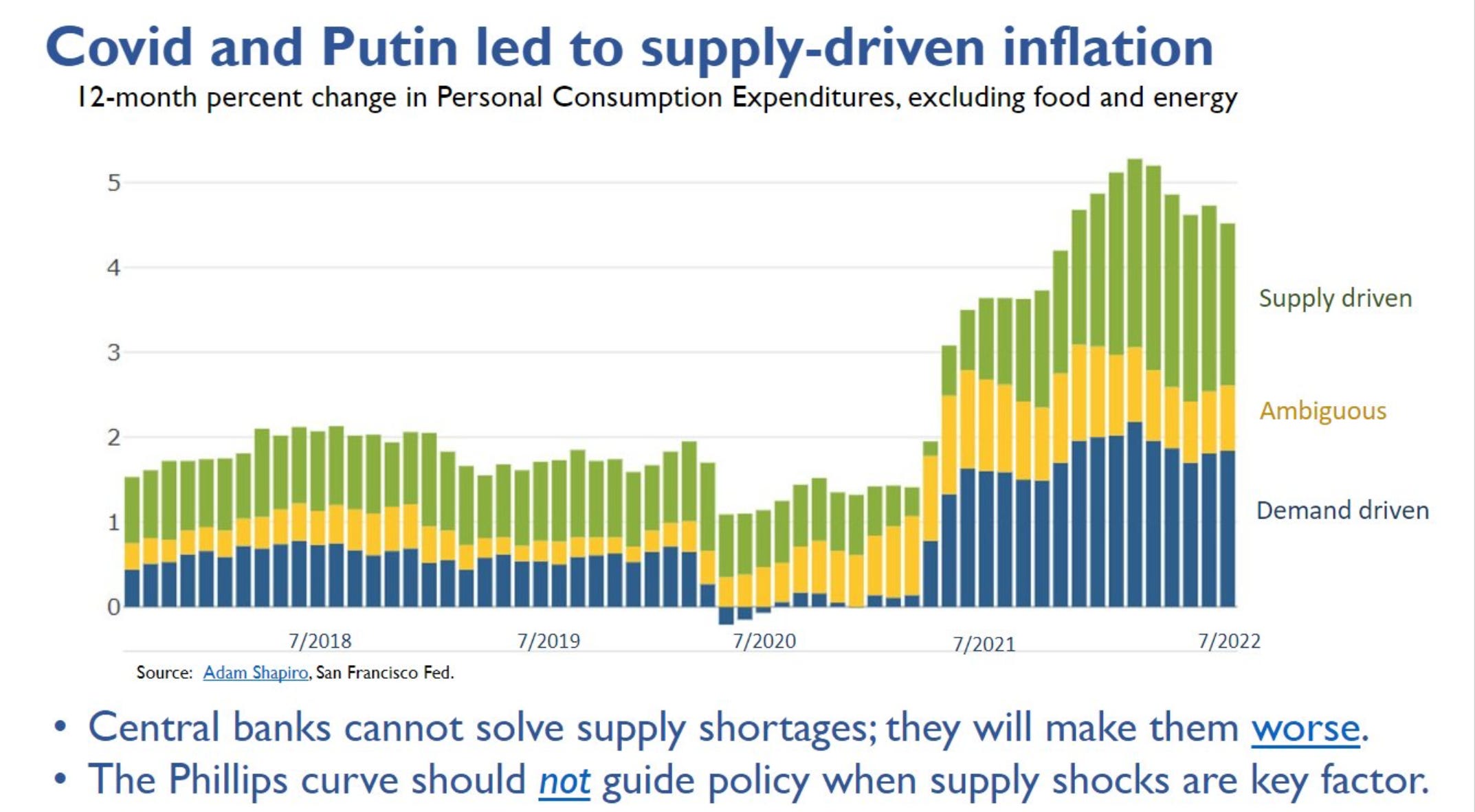

unfortunately, when the fed's own research estimates that about half of present inflation is supply driven (not demand-driven), it's not obvious that softening the labor market will have any of the desired effect. when it doesn’t, we’ll find ourselves saddled with stagflation, higher unemployment, and much less ability to buy a house or car (at least for those paying with credit rather than cash).

simply put: the fed cannot solve today’s supply-driven inflation. the global economy is operating well below the capacity it would otherwise be at if covid had not occurred and if russia had not invaded ukraine. covid supply messes are nowhere near to being resolved, and the war in ukraine continues to prevent historically significant quantities of food and energy from reaching the rest of the world.

9/30 edit: claudia sahm published this talk on the above-mentioned sf fed paper a few days after i first published this post. give her talk and summary tweet thread a look.

image 1: from shapiro, 2022, “How Much Do Supply and Demand Drive Inflation?” title and bullet points are from claudia sahm’s recent presentation to the institute for macroeconomic policy in berlin.

the solutions we need to present inflation are fiscal, not monetary. the chips bill, inflation reduction act, and the science act have laudable intended effects but they won't show up for years, if not decades. we need immediate action by congress to use the power of the purse to buffer supply chains beyond what they've done for petrol. that means moving to radically upzone across the country to create more housing supply; it means creating similar buffer stocks for core food supplies; it means making long-term commitments to buy commodities used to make appliances and autos at fixed rates to enable suppliers to manage through price volatility; it means negotiating and managing the cost of medicine through tighter regulation, and of higher education by redirecting federal money directly to schools rather than in pseudo-loans to students that will ultimately get forgiven down the line. most importantly, it means managing a buffer stock of public work (via something like a jobs guarantee program) so that softening the private labor market need not cause unemployment, just a shift from private to public payrolls.

it means, in short, taking a more active hand in the market. if we're too afraid to use our representative democracy to thoughtfully pick some winners and losers in the economy, an increasingly smaller percentage of the population will keep winning (by r>g logic) and the rest will keep losing. the 21st century will either be a century of continued stagnation, increased inequality, political foment, and decline; or it will be one where the bulwark of public fiscal power is finally erected against the erosion of human potential left by the last five decades of failure in the private market’s ability to improve the public good.

the future is one of price volatility. a warming and unstable climate will cause more disease transmission from non-human to human animals as populations of both migrate fight for more habitable surfaces on earth, pushing up against one another. this will cause more supply-chain-disrupting pandemics. extreme weather will cause more droughts and food supply volatility. economic and technological stagnation will cause political autarky, which will put more friction in supply chains as nations hoard supplies and increase tariffs. pressure to green our energy and transportation systems will outpace our capacity to meet that demand and drive up commodity prices—which will in turn spill over into the price of most durable goods. stagnating or falling birth rates will lead to declining population which will make labor markets tighter and contribute to slowing global growth (less people; less demand).

central banks’ toolkits are blunt. they are best suited to solve broad-based liquidity challenges. this century’s inflationary pressures are going to be driven in large part by secular supply shocks. the federal reserve is not currently equipped to solve these unless they occur in the financial system. congress has to understand that price stability and full employment is a full federal job—fed, congress, and treasury must coordinate. and ultimately because these authorities all issue from congress (and from us), price stability and full employment are our responsibility as voters in federal elections. the recent legislative successes are steps towards this future, but we need to do more, but if we celebrate too early we risk falling back into our old pattern. price stability and full employment is everyone’s job.